2023 – Capital demands dent performance

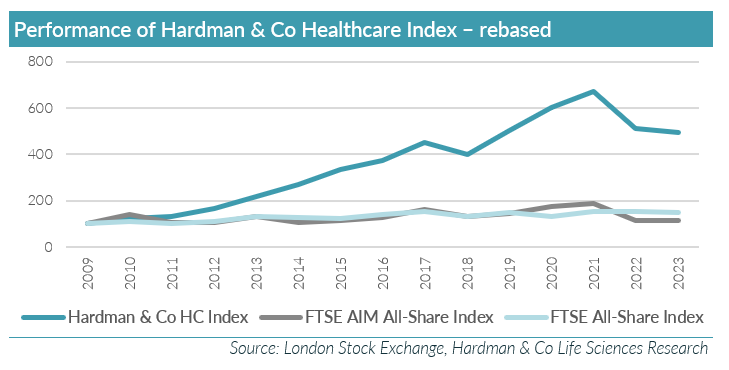

The Hardman & Co Healthcare Index (HHI) has been running since 2009. Its main function is to highlight the attractions of life sciences investments over the long term. For the second year running, apart from global economic influences affecting world markets, performance in 2023 was dented by the capital-intensive nature of the sector. The HHI fell 3.7%, to 483.8, underperforming the main London markets – FTSE 100 (+3.8%) and FTSE All-Share (3.8%) but outperforming the FTSE AIM All-Share Index (-8.2%). Only 15 companies in our index saw share prices rise in 2023, four of these benefiting from trade sales. Despite challenges in raising new capital from the market, 15 companies (29%) did achieve successful outcomes. A number of companies are short of cash and will need more capital in order to get auditors to sign off their accounts – so 2024 looks as though it will be busy again.

- Despite setbacks over the past two years, since inauguration in 2009, the CAGR for the HHI has been 12.0%, compared with 3.3% for the FTSE All-Share Index and 0.5% for the FTSE AIM All-Share Index, highlighting the attractiveness of the healthcare sector as a long-term investment, despite being capital-intensive.

- Of the 52 companies included in the HHI, only 15 recorded an increase in their share prices in 2023, four benefiting from M&A activity. One marked time (change <0.5%) and the remaining 36 companies recorded falls.

- The variance between the best- and worst-performing stocks was in line with historic data, at 223% – hVIVO (HVO) rising 138% and Advanced Oncotherapy (AVO) down 86% at the time of being suspended; the median share price change was -20%.

- In relative terms, 17 stocks outperformed the index during 2023, with the other 35 underperforming.

- After two really good years in 2020 and 2021, biotech and healthcare stocks had become overvalued, as evidenced by a marked reduction in M&A activity. Since then, along with global markets in general, biotech and healthcare stocks have been re-rated downwards. In addition, the trend towards greater risk-aversion in response to geopolitical events, higher inflation and higher interest rates have made it more difficult to raise capital over the past two years.