GSK’s announcement, on 14 May 2025, that it is to acquire efimosfermin ‒ the lead asset of Boston Pharmaceuticals (Boston) being developed for the treatment and prevention of liver disease ‒ has attracted much media attention, even making BBC news headlines on subsequent days. This decision is based on Phase II data, published in 4Q’24, with GSK agreeing to pay $1.2bn upfront for efimosfermin, and further success-based development milestones of up to $800m. GSK will be responsible also for success-based milestone payments and tiered royalties that become due to Novartis.

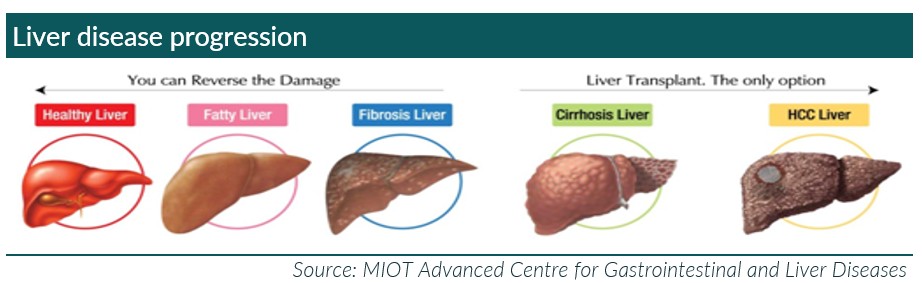

Given the high prevalence of obesity in the world and increasing alcohol-related issues, there has been an enormous rise in the number of patients with liver disease. “Liver disease” is a composite term describing >100 conditions that may be inherited, degenerative (e.g. cancers), or caused by lifestyle factors and infectious agents. Cirrhosis is the end-stage result of liver fibrosis, which occurs when scar tissue accumulates from chronic liver damage. Patients with established cirrhosis are at risk of hepatocellular carcinoma (HCC): up to 90% of HCC patients have cirrhosis.

Efimosfermin is a once-monthly, subcutaneously injected, fibroblast growth factor 21 (FGF21) analogue in clinical development for the treatment of metabolic dysfunction-associated steatohepatitis (MASH), including cirrhosis, and future development in alcohol-related liver disease (ALD). In addition to targeting the main forms of liver disease in its various stages with efimosfermin, GSK is aiming to maximise this putative drug’s potential by combining its direct anti-fibrotic mechanism of action with its own drug, GSK’990, a siRNA therapeutic in development, for other subsets of patients with liver disease.

Boston presented Phase II data at the American Association for the Study of Liver Diseases (AASLD) in November 2024. In a randomised, double-blind, placebo-controlled Phase II study (n=84), the efficacy and safety of once-monthly efimosfermin ‒ 300 mg dosed subcutaneously ‒ was assessed in patients with biopsy-confirmed F2 or F3 MASH, over a period of 24 weeks.

On the back of this data, Boston was expecting to advance the clinical programme into Phase III, late-stage development, in 2025. However, as is often seen when major companies acquire the rights to products, GSK might determine that a further confirmatory Phase II trial is needed before committing to expensive Phase III trials. In the event that this does occur, these timescales would get extended.

So, on the face of it, GSK has done a good deal: efimosfermin has completed a Phase II trial in which it was shown to be reasonably efficacious across key liver and metabolic biomarkers; it is targeting a large and growing patient population with various stages of liver disease where the end-game, if left untreated, is an expensive and complex liver transplant; and it might be used in combination with GSK’s own development product to maximise the commercial opportunity.

First, even if the timescales alluded to by Boston remain unchanged, the recruitment and running of a double-blind placebo-controlled Phase III trial in a reasonable number of patients (say 300 equally divided between efimosfermin and placebo) and followed up for six months, will take an estimated 2.5 years (end-2027). This will be followed by 12 months with the regulators, suggesting the earliest that it will be launched is 2029. So, what will the market look like then?

The current landscape for patients with liver disease is changing rapidly. The most common form of the disease, fatty liver or non-alcoholic steatohepatitis (NASH), is closely associated with obesity, which also brings into play other conditions, including diabetes and cardiovascular disease. Patients with fatty liver are far more likely to die from other causes, particularly cardiovascular events. The introduction of glucagon-like peptide-1 (GLP-1) receptor agonists for the treatment of obesity is having a significant impact on the market for liver disease, not only improving fatty liver but also many other conditions. GLP-1 analogues decrease the risk of fatty liver and, consequently, reduce the risks of associated conditions and are, therefore, are changing the commercial landscape. Additionally, there are a number of other drugs for fatty liver that have either been approved or are nearing approval.

There are calls for GLP-1 analogues to be used far more widely, in the same way that statins have become widely prescribed for the prevention of cardiovascular risk; albeit, this would put significant pressure on the payors. However, this would be a small price to pay compared with the costs of hospitalisation for associated diseases caused by obesity.

Novo Nordisk lowered Ozempic growth recently, largely due to its poor decision to allow compounded equivalents to enter the market when there was a supply shortage. But Mounjaro (Lilly) continues to gain market share and looks set to become the #1 GLP-1 analogue in 2025. The table below shows the anticipated market progression of GLP-1 analogues and that GSK will be facing a very tough and established commercial landscape when it comes to the launch of efimosfermin.

Opinions in this article are solely those of our Life Sciences analyst.